Not trying to nitpick, but there are a lot of posts thrown around on this site with an heir of authority as if they were factual when infact they are just opinion.

Neophyte, I see your above post as one of these…

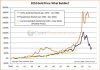

We are at an interesting point, I think to completely dismiss the idea that prices will correct is naïve as it would be to completely write off the possibility they will stagnate then rise again. Personally though I am leaning towards the expectation that prices will correct back to historical norms.

* http://www.tanyaplibersek.fahcsia.gov.au/mediareleases/2009/Pages/home_owners_boost_05dec09.aspx

Neophyte, I see your above post as one of these…

What are you basing this 8%+ figure on? Is there mathematical reasoning behind it? Does it have historical precedence/relevance? Or was it just pulled out of a hat?In Australia the potential cause of house price crash is mass unemployment at least 8%+. Unless people lose their jobs its unlikely they will lose their homes.

Once again, what are you basing the 1-2% figure on? My opinion is that we could be at the tipping point for many of the 190,000* FHBs that took it up during the “boost” period (Oct 2008 to Dec 2009) where we had record low interest rates available and free large deposits. Many leveraged to the hilt (as proven by the high LVR reported in the Fujitsu reports) which indicated poor level of savings and most banks only factor in around a 1.5% interest rate buffer, which has already likely been breached in the 6 official rate rises since October and most banks increasing over the official cash rate during this period. Not to mention we have seen other expenses increase significantly over the same time, including fuel costs which could be affecting those in the mortgage belt suburbs…Rising interest rates cause belt-tightening, however they are also only a temporary measure (e.g. 1-2 years to stop inflation) and at the same time inflation => wage growth. For people to be unable to meet there mortgages rates need to rise at least another 1-2% maybe more, however that can only happen if the economy is booming.

Fujitsu’s mortgage updates indicate quite a large number of new buyers have been affected in what they measure as “mortgage stress”. Thing is that it only needs to be a small fraction of stressed sellersr that can cause prices to dip or crash because it’s only ever a small fraction of the entire market that is for sale each year…Undoubtedly some people are at risk, but they are a very small fraction comprising those who have both bought recently, have low job security and overextended.

I do agree with the above. I would assume most that have owned for 3 years are in a much better position than those that have purchased more recently, but then for those that have equity behind them it’s less of a concern if they have to knock 5% off asking price to compete with distressed stock…Most people are not on a financial knife-edge. If you bought more than 3 years ago then your income has probably gone up 10% since and your property value has probably gone up 20%.

We are at an interesting point, I think to completely dismiss the idea that prices will correct is naïve as it would be to completely write off the possibility they will stagnate then rise again. Personally though I am leaning towards the expectation that prices will correct back to historical norms.

* http://www.tanyaplibersek.fahcsia.gov.au/mediareleases/2009/Pages/home_owners_boost_05dec09.aspx