In the eyes of foreigners:

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

And try buying off the plan. Even when it's expensive there's a long queue and you need to pay a nonrefundable $5k reservation fee just to have a look!

) on Marsden Park * Ropes Crossings to become another profitable suburbs like Schofileds, Kellyville and Baulkham Hills.

) on Marsden Park * Ropes Crossings to become another profitable suburbs like Schofileds, Kellyville and Baulkham Hills.Yes, that's the thing. the land was offered by www.Landcom.com.au in Airds, but now is no more avaialble, due to the people queueing like there is no tomorrow.

I'm now waiting (or betting

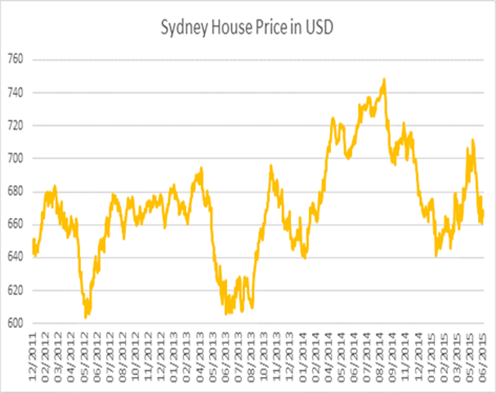

Fingers crossed and looking at the graph that you submitted above, it confirms that buying the house in newly openedarea will soon appreciates due to land scarcity.

I'm ready and open to be humbled by anyone here if there is anything that I say above is wrong.

Indeed."BayView, had skin in the game, but it was a failure and he had to sell a bunch of properties, take that into account when considering his opinion or advice..."

Who would you rather listen to; someone who has done nothing and not gained the experience (good or bad), or someone who has had a crack and done ok, but also stuffed up a lot of things, and now can give you the benefit of that experience?

Oh no it doesn't.....This chart tells the story really.

As we keep telling you; affordability is relative.On the business of property investing, your experience is likely useful to learn from, on the topic of housing affordability your experience means very little (i.e. it is not relevant).

Providing some anecdotal experiences of your own does nothing to refute the facts on affordability laid out by myself and others over the years.

As usual your posts miss the point. People buy (i.e. afford) Ferrari's, but it doesn't mean they are an affordable car. Affordability is a scale and homes are much less affordable over the last 10-15 years than they were in the decades prior.So just to re-iterate - EVERY MONTH 7000+ FHBers ARE ABLE TO AFFORD A HOUSE!!!!!

Deposit on what?Do you deny that a higher price to income ratio increases the time & effort required to save a deposit?

Last month 7000 families didn't care much about that.As usual your posts miss the point. People buy (i.e. afford) Ferrari's, but it doesn't mean they are an affordable car. Affordability is a scale and homes are much less affordable over the last 10-15 years than they were in the decades prior.

The month before 8000 FHBers didn't care about that hypothetical point either.Do you deny that prices have risen well above that of a median income (or even household income)?

Back in Jan there were another 8000 FHBers that overcame adversity & saved for a deposit.Do you deny that a higher price to income ratio increases the time & effort required to save a deposit?

8000 FHBers for every month of 2014 didn't think it was a biggie.....Do you deny that periods with higher inflation and wage growth make it faster for the real value of a mortgage to fall (hence easier to repay over the life of a loan even if as difficult to begin with)?

Another 7000 anecdotal examples reared their ugly head every single month of 2013 too - they all decided that they were prepared to ignore macrobusiness & hobos charts & take the risk of buying a shelterDo you deny that in an example where prices are doubled, but interest rates halved, that the buyer ends up worse off (repaying more & taking a greater level of risk) assuming the same nominal repayments?

The ABS graph for the last 25 yrs clearly shows 7-8000 FHBers being able to afford a house every month.The number of first home buyers does not disprove the fact that housing affordability is worse.

The ABS graph for the last 25 yrs clearly shows 7-8000 FHBers being able to afford a house every month.

That's about a sample size of over 1,000,000 families.

Surely that is sufficient to convince you that affordability is pretty much the same as 25 yrs ago.

I guess the 6 million more people (circa 2 million more households) added to Australia since the beginning of that chart have no bearing whatsoever. LOL.The ABS graph for the last 25 yrs clearly shows 7-8000 FHBers being able to afford a house every month.

Every day another 400 families can afford to buy a 1st home. Housing remains affordable - when it stops being affordable, people will stop buying & price will stop rising. Based on the trend of the last 25 yrs do you think it will be any time soon ?I guess the 6 million more people (circa 2 million more households) added to Australia since the beginning of that chart have no bearing whatsoever. LOL.

Strawman.It's 2050, Australia's population has increased to 35 million, house pricses have doubled again relative to incomes (now 20x), but lookout here's keithj to tell us that there's still 7,000 first home buyers, so property affordability remains unchanged from 2015.

Strawman.Every day another 400 families can afford to buy a 1st home. Housing remains affordable - when it stops being affordable, people will stop buying & price will stop rising. Based on the trend of the last 25 yrs do you think it will be any time soon ?

As usual your posts miss the point. People buy (i.e. afford) Ferrari's, but it doesn't mean they are an affordable car. Affordability is a scale and homes are much less affordable over the last 10-15 years than they were in the decades prior.

Do you deny that prices have risen well above that of a median income (or even household income)?

Do you deny that a higher price to income ratio increases the time & effort required to save a deposit?

Do you deny that periods with higher inflation and wage growth make it faster for the real value of a mortgage to fall (hence easier to repay over the life of a loan even if as difficult to begin with)?

Do you deny that in an example where prices are doubled, but interest rates halved, that the buyer ends up worse off (repaying more & taking a greater level of risk) assuming the same nominal repayments?

Even before I read Jerrybee's post above, I wanted to suggest to Hobo-jo that FHBs do not buy median homes. They are poor, not like us investors with our hundreds of thousands of dollars of equity buying up above-median PPORs. I thought they tend to buy below median homes so maybe, just maybe, the stats about median prices vs incomes is not relevant.

What do we think about that?

Prices have gone up everywhere, in the median suburbs, in the expensive suburbs, in rural towns and in "cheap" suburbs... take Elizabeth for example (in Adelaide), outer suburbs, daggy area, entry level, median price in 2000 was $60,000, last year it was $230,000. Do you think FHB wages have risen by 300% over the last 15 years?Even before I read Jerrybee's post above, I wanted to suggest to Hobo-jo that FHBs do not buy median homes. They are poor, not like us investors with our hundreds of thousands of dollars of equity buying up above-median PPORs. I thought they tend to buy below median homes so maybe, just maybe, the stats about median prices vs incomes is not relevant.

What do we think about that?