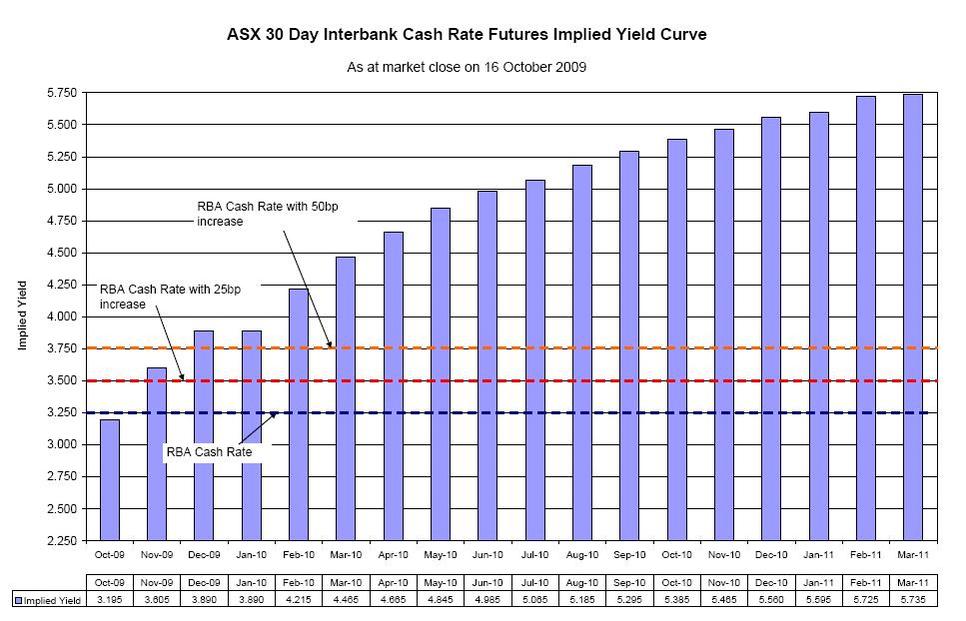

Glenn Stevens speech of 15th Oct caused the market & economists to rethink their Cash Rate expectations for 2010.

It's starting to look like we'll have +1.5% over the next 6 months, and a further +0.5% by this time next year....

...that'll mean a SVR of ~8% (or 7.25% after pro-pack discount) in Oct 2010. And the market isn't expecting it to stop there, with further rises likely. By then I'd expect the rest of the world (US & Europe) to be in recovery mode.

However, some economists see good reasons for a pause in rates in mid 2010. Westpac has recently upgraded its IR expectations, but not as high as the market expects....

The big banks have not committed to follow the RBA, they've reserved the right to increase more.

So, the question is.... what's the highest the SVR will get to in 2010 ?

It's starting to look like we'll have +1.5% over the next 6 months, and a further +0.5% by this time next year....

...that'll mean a SVR of ~8% (or 7.25% after pro-pack discount) in Oct 2010. And the market isn't expecting it to stop there, with further rises likely. By then I'd expect the rest of the world (US & Europe) to be in recovery mode.

However, some economists see good reasons for a pause in rates in mid 2010. Westpac has recently upgraded its IR expectations, but not as high as the market expects....

The market has a better track record than the economists.Westpac said:

- After the cash rate reaches 4.5% the standard variable mortgage rate will be around 7.3%. In the previous rate hike cycle we found that once the SVMR exceeded 7% households were extremely sensitive to rate hikes......

- Previous housing recoveries have been largely driven by demand and the supply of credit has adjusted to accommodate demand. In this recovery the supply of credit will be a significant constraint.....

...

- Debt servicing ratios for Australia’s household sector will rise quickly.....

The big banks have not committed to follow the RBA, they've reserved the right to increase more.

So, the question is.... what's the highest the SVR will get to in 2010 ?

")