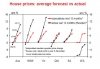

I've seen some posts skeptical of a 2009 FHB bubble, so I put some figures to paper and came up with the below:

Jane & Johnny

Income $35k pa (each), $30k net ($2500 pm, $5k net combined pm)

In all scenarios $7k will be subtracted from deposit for stamp duty/costs to borrow/pest & building inspection

Borrowing Calculator Used: http://www.aussie.com.au/home-loan/calculators/borrowing-calculator.htm

Rates Used From: http://www.loansense.com.au/historical-rates.html

25 Year Loan Term Used For Example

July 2007

Rate: 8.05%

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 100%

Serviceability Allows: $347k

Deposit Allows: $N/A

Purchasing Power (Including Deposit): $362k

July 2008

Rate: 9.45%

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 100%

Serviceability Allows: $312k

Deposit Allows: $N/A

Purchasing Power (Including Deposit): $327k

July 2009

Rate: 5.55%

Saved Deposit: $15k

FHOG: $14k (-$7k costs)

Total Deposit: $22k

LVR: 95%

Serviceability Allows: $429k

Deposit Allows: $418k

Purchasing Power (Including Deposit): $440k

January 2010

Rate: 6.66% (using Dec rate)

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 95%

Serviceability Allows: $389k

Deposit Allows: $285k

Purchasing Power (Including Deposit): $300k

What effect would the Westpac 87% max LVR have on this couple if they were new to the bank?

January 2010

Rate: 6.66% (using Dec rate)

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 87%

Serviceability Allows: $389k

Deposit Allows: $115k

Purchasing Power (Including Deposit): $130k

Some other figures:

Approximately 30% of housing finance in mid 2009 was provided to FHBs, that dropped to 20% by years end and with the FHOG reduced further Jan 1st 2010 it will continue to fall (IMO).

Approximately 50% of FHBs in mid 2009 were borrowing with LVRs above 90%.

I haven't tried to twist the figures to make them work out this way, I honestly just picked a couple of average looking wages and used the first figures I came up with. Feel free to counter them with your own if you think you can provide a more reasonable scenario...

Someone on Hot Copper mentioned the stamp duty costs were too high and that they are very low/non-existent for FHBs, so here are the 2009/2010 examples again with $3k costs:

July 2009

Rate: 5.55%

Saved Deposit: $15k

FHOG: $14k (-$3k costs)

Total Deposit: $26k

LVR: 95%

Serviceability Allows: $429k

Deposit Allows: $494k

Purchasing Power (Including Deposit): $455k

January 2010

Rate: 6.66% (using Dec rate)

Saved Deposit: $15k

FHOG: $7k (-$3k costs)

Total Deposit: $19k

LVR: 95%

Serviceability Allows: $389k

Deposit Allows: $361k

Purchasing Power (Including Deposit): $380k

Obviously the figures are a little closer in this example due to the 2009 buyers hitting the serviceability limit before the deposit limit.

Investors are going to have to do a lot of buying to fill the hole that these FHBs are leaving/have left...

How would the purchasing power look with further increase in interest rates or a 90% LVR becoming the norm as the banks tighten up their lending?? Do the figures and work it out")

Jane & Johnny

Income $35k pa (each), $30k net ($2500 pm, $5k net combined pm)

In all scenarios $7k will be subtracted from deposit for stamp duty/costs to borrow/pest & building inspection

Borrowing Calculator Used: http://www.aussie.com.au/home-loan/calculators/borrowing-calculator.htm

Rates Used From: http://www.loansense.com.au/historical-rates.html

25 Year Loan Term Used For Example

July 2007

Rate: 8.05%

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 100%

Serviceability Allows: $347k

Deposit Allows: $N/A

Purchasing Power (Including Deposit): $362k

July 2008

Rate: 9.45%

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 100%

Serviceability Allows: $312k

Deposit Allows: $N/A

Purchasing Power (Including Deposit): $327k

July 2009

Rate: 5.55%

Saved Deposit: $15k

FHOG: $14k (-$7k costs)

Total Deposit: $22k

LVR: 95%

Serviceability Allows: $429k

Deposit Allows: $418k

Purchasing Power (Including Deposit): $440k

January 2010

Rate: 6.66% (using Dec rate)

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 95%

Serviceability Allows: $389k

Deposit Allows: $285k

Purchasing Power (Including Deposit): $300k

What effect would the Westpac 87% max LVR have on this couple if they were new to the bank?

January 2010

Rate: 6.66% (using Dec rate)

Saved Deposit: $15k

FHOG: $7k (-$7k costs)

Total Deposit: $15k

LVR: 87%

Serviceability Allows: $389k

Deposit Allows: $115k

Purchasing Power (Including Deposit): $130k

Some other figures:

Approximately 30% of housing finance in mid 2009 was provided to FHBs, that dropped to 20% by years end and with the FHOG reduced further Jan 1st 2010 it will continue to fall (IMO).

Approximately 50% of FHBs in mid 2009 were borrowing with LVRs above 90%.

I haven't tried to twist the figures to make them work out this way, I honestly just picked a couple of average looking wages and used the first figures I came up with. Feel free to counter them with your own if you think you can provide a more reasonable scenario...

Someone on Hot Copper mentioned the stamp duty costs were too high and that they are very low/non-existent for FHBs, so here are the 2009/2010 examples again with $3k costs:

July 2009

Rate: 5.55%

Saved Deposit: $15k

FHOG: $14k (-$3k costs)

Total Deposit: $26k

LVR: 95%

Serviceability Allows: $429k

Deposit Allows: $494k

Purchasing Power (Including Deposit): $455k

January 2010

Rate: 6.66% (using Dec rate)

Saved Deposit: $15k

FHOG: $7k (-$3k costs)

Total Deposit: $19k

LVR: 95%

Serviceability Allows: $389k

Deposit Allows: $361k

Purchasing Power (Including Deposit): $380k

Obviously the figures are a little closer in this example due to the 2009 buyers hitting the serviceability limit before the deposit limit.

Investors are going to have to do a lot of buying to fill the hole that these FHBs are leaving/have left...

How would the purchasing power look with further increase in interest rates or a 90% LVR becoming the norm as the banks tighten up their lending?? Do the figures and work it out