Lizzie, you are arguing for an appeal to authority. It doesn't matter if Jesus himself came down and said there was a shortage, I'd still ask him for figures and facts to back up his claim.

I am regarding a loss being "all of my costs were greater than all of my income on this property" as reported to the ATO.

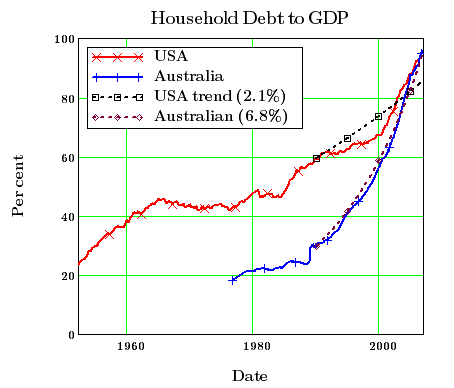

This will affect our consumer economy. We already spend $105 for $100 we earn, we *need* this borrowing to keep our economy growing. Without it we'd be in recession. We borrow our way out of recession each year.

This will have downward pressure on prices.

We have 100% loans. This is to demonstrate borrowing power - if you had 20k deposit, and 80% loans, you could only borrow 100k. If it's 90% you can borrow 200k, 95% = 400k. We're already at 105%

This is overwhelmingly a paper gain in house prices and can only be realised if other Australians take out debt to buy the house off them.

2/3's have a PAPER LOSS. Not necessarily an actual cash loss. I'm one of those. Running at a paper loss but a cash positive position is the point of maximum tax efficiency for many investors. Do you understand the difference?

I am regarding a loss being "all of my costs were greater than all of my income on this property" as reported to the ATO.

e) Reduce spending on junk before reducing spending on a house.

This will affect our consumer economy. We already spend $105 for $100 we earn, we *need* this borrowing to keep our economy growing. Without it we'd be in recession. We borrow our way out of recession each year.

f) Downsizing houses. Kids sharing bedrooms (as was common only a few decades ago - I was one!). Taking in boarders.

This will have downward pressure on prices.

100% low-doc IO loans? I highly doubt there are many of those in Australia,

We have 100% loans. This is to demonstrate borrowing power - if you had 20k deposit, and 80% loans, you could only borrow 100k. If it's 90% you can borrow 200k, 95% = 400k. We're already at 105%

Also, didn't the average Australian increase their net wealth from $250k to $300k recently? What does that enable people to do?

This is overwhelmingly a paper gain in house prices and can only be realised if other Australians take out debt to buy the house off them.

i have no idea what you just said but i think i know what you are getting at. okay - i just called my pm to ask the vacancy rate in newcastle and she advised me it was around 1%. would you like me to call another pm and confirm this? this 1% is usually the really (bleep) houses, boarding house rooms, units that no one wants to live in - so the demand for reasonable rental accomodation is huge. demand and supply means i can ask more for my property. according to you, this is a good thing because it means the yield is more in line with the property price.

i have no idea what you just said but i think i know what you are getting at. okay - i just called my pm to ask the vacancy rate in newcastle and she advised me it was around 1%. would you like me to call another pm and confirm this? this 1% is usually the really (bleep) houses, boarding house rooms, units that no one wants to live in - so the demand for reasonable rental accomodation is huge. demand and supply means i can ask more for my property. according to you, this is a good thing because it means the yield is more in line with the property price.