RBA comments

He added: "In dollar terms, Sydney is still way, way more expensive than anywhere else in Australia, and I think it's so expensive that, particularly for a lot of young people, it's in their interests to go elsewhere, where the lifestyle is more affordable."

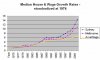

Mr Macfarlane said it was "too expensive to live in NSW" and presented evidence showing that house prices in Sydney were almost double the average for the rest of Australia at the peak of the property boom in 2002. Even though the gap had narrowed recently, Sydney prices were still two-thirds higher than the average house price for other capitals.

He added: "Sydney house prices are somewhere between 50 and 60 per cent more expensive than Melbourne house prices."

The Reserve Bank this week published figures showing average Sydney home prices were almost 10 times average annual earnings in the state, compared with seven times in Melbourne and a little over six times in Brisbane and Canberra.

Anyone have any historical data on housing affordability across the country????

He added: "In dollar terms, Sydney is still way, way more expensive than anywhere else in Australia, and I think it's so expensive that, particularly for a lot of young people, it's in their interests to go elsewhere, where the lifestyle is more affordable."

Mr Macfarlane said it was "too expensive to live in NSW" and presented evidence showing that house prices in Sydney were almost double the average for the rest of Australia at the peak of the property boom in 2002. Even though the gap had narrowed recently, Sydney prices were still two-thirds higher than the average house price for other capitals.

He added: "Sydney house prices are somewhere between 50 and 60 per cent more expensive than Melbourne house prices."

The Reserve Bank this week published figures showing average Sydney home prices were almost 10 times average annual earnings in the state, compared with seven times in Melbourne and a little over six times in Brisbane and Canberra.

Anyone have any historical data on housing affordability across the country????

") ).

).